Latest update on July 02, 2026

[cg_add-class=heading-style-h4]In a Nutshell

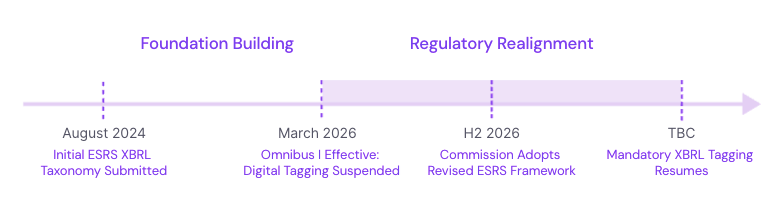

- Mandatory XBRL tagging of sustainability reports under CSRD is currently suspended by Directive (EU) 2026/470 (in force 18 March 2026), until the ESEF Delegated Regulation (2019/815) is updated.

- Update August 2024 (historical): the draft taxonomy developed by EFRAG was submitted to the European Commission and the European Securities and Markets Authority (ESMA) — that draft sits in the queue awaiting ESEF rules.

- The ESRS XBRL Taxonomy comprises a set of XBRL elements ("tags") and reflects the structure of the ESRS standards (cross-cutting standards and topical ESG standards).

- Once tagging resumes, the digital data points will enable real-time external analysis and auditing — supporting both reporters and the users of sustainability information.

NOTE: Status as of July 2026

Mandatory XBRL tagging of sustainability reports is currently suspended. Directive (EU) 2026/470 (Omnibus I, in force 18 March 2026) amends CSRD Article 29d to provide:

Until such rules on the marking-up are adopted by way of [Delegated Regulation (EU) 2019/815], undertakings shall not be required to mark up their sustainability reporting.

In practice this means Wave 1 reporters preparing FY 2025 and FY 2026 sustainability statements continue to prepare them in single electronic reporting format (ESEF), but are not required to tag the sustainability portion. Member States may also waive the collective board responsibility for digital marking-up (amended Article 33(1)).

This article preserves the underlying concept — what the XBRL taxonomy does, how it's structured, what tagging looks like in practice — so you can review it ahead of when mandatory tagging resumes. The path to resumption (Commission revised ESRS delegated act → ESEF amendment cycle) is described in the "Outlook" section at the end.

The European Union (EU) has been advancing its sustainability agenda through the European Sustainability Reporting Standards (ESRS). At the heart of this framework sits the ESRS Data Point List and the ESRS XBRL tagging system, which together define how sustainability data is structured and communicated.

The XBRL tagging system was developed under the leadership of the European Financial Reporting Advisory Group (EFRAG). A first draft version of the digital taxonomy for the published ESRS (Set 1) was published on 8 February 2024 and, after several Q&A sessions, was submitted to the European Commission and ESMA as a final draft in August 2024.

On the Commission's side, the original plan was for ESMA to draft the technical tagging standards (RTS) and for the Commission to adopt the rules as a delegated act amending Delegated Regulation (EU) 2019/815 on the European Single Electronic Format (ESEF). That process is what Omnibus I has now placed on hold for sustainability information specifically — until the ESEF rules are updated, mandatory mark-up does not apply.

Two things follow from this. First: the August 2024 draft taxonomy is not the operative legal instrument — it is a historical artefact awaiting ESEF amendment. Second: the draft was built against the original 2023 ESRS architecture, which the November 2025 EFRAG draft of ESRS 2 consolidates (per-topic MDR-P/A/M/T becomes a single GDR-P/A/M/T set under ESRS 2). The taxonomy will need rework before any future adoption.

With that context, the rest of this article walks through the concept — what XBRL is, what the ESRS XBRL Taxonomy looks like, how tagging works in practice — so that you can review the mechanics ahead of when mandatory tagging resumes.

ESRS XBRL Taxonomy: The Basics

What is the ESRS XBRL Taxonomy?

XBRL stands for Extensible Business Reporting Language. It is a standardised way to flow structured information from the preparer to the user. You can picture XBRL as a modular system of individual reporting elements ("tags") for the digital reporting of company information. For specific reporting purposes, templates are developed that describe the relevant elements and their relationships — these are called taxonomies.

EFRAG was assigned the responsibility of developing an XBRL Taxonomy that reflects the ESRS, so that companies can — when the regime is operative — categorise sustainability data in a structured, machine-readable manner.

With the ESRS XBRL taxonomy, companies reporting under the CSRD will (once tagging resumes) tag and digitalise their sustainability disclosures.

The taxonomy uses Extensible Markup Language (XML) as its foundation. XML is widely used in financial reporting as a way to structure business information in a digitally accessible format.

Who Needs to Implement the ESRS XBRL Tagging and Why is it Important?

Under the original CSRD regime, companies in CSRD scope would have been required to implement XBRL tagging to transform their sustainability disclosures into a computer-understandable format. Omnibus I suspends that obligation for now — but the underlying purpose has not gone away.

A machine-readable XBRL taxonomy marks a substantial step toward making sustainability reporting digitally accessible and useful — for analysts, regulators, auditors and other report users.

By separating the individual disclosure items from the narrative legal text of the ESRS, digital XBRL tagging would simplify automated analysis and reduce redundancies and manual errors during data transformation. Standardised digital data points can be made accessible for external analysis and auditing in real time, while also serving as a basis for reporters to tell their own sustainability story in their narrative reports.

ESRS XBRL Taxonomy Structure Explained

The ESRS XBRL taxonomy represents the architecture and content of the standards in a digital format. It mirrors the structure of the ESRS: the two cross-cutting standards (ESRS 1 and ESRS 2) and the ten topical standards covering Environmental (E), Social (S) and Governance (G) topics.

An important aspect of the taxonomy is its emphasis on the interrelation between the cross-cutting and topical ESG standards — for example, linking general requirements with specific targets, policies or metrics in the topical standards.

Understanding the Frame and Structure

To navigate the taxonomy, it helps to know the content and structure of the ESRS Disclosure Requirements that are converted into digital XBRL elements:

- Cross-cutting standards

- ESRS 1 (General Requirements)

- ESRS 2 (General Disclosures)

- ESG topical standards

- ESRS E1-E5: ESRS E1 (Climate change), ESRS E2 (Pollution), ESRS E3 (Water and marine resources), ESRS E4 (Biodiversity and ecosystems), ESRS E5 (Circular economy)

- ESRS S1-S4: ESRS S1 (Own workforce), ESRS S2 (Workers in the value chain), ESRS S3 (Affected communities), ESRS S4 (Consumers and end-users)

- ESRS G1 (Business conduct)

Overview of XBRL Digital Elements

Cross-cutting standard ESRS 2 (General Disclosures)

ESRS 2 sets the general level of information that companies must provide across the topical ESG standards.

In the August 2024 EFRAG draft, the content of ESRS 2 in the taxonomy is divided into:

- General Disclosure Requirements that correspond to the Disclosure Requirements (DRs) related to Basis for Preparation (BP), Governance (GOV), Strategy (SBM) and Impact, Risk and Opportunity management (IRO).

- Minimum Disclosure Requirements (MDR) that correspond to MDRs on Policies (MDR-P), Actions (MDR-A), Targets (MDR-T) and Metrics (MDR-M). In the August 2024 draft, the MDRs act as a centralised table structure for presenting information for material topics across the topical ESRS.

Important to note: the November 2025 EFRAG draft of ESRS 2 consolidates the per-topic MDR-P/A/M/T into four cross-cutting General Disclosure Requirements (GDR-P, GDR-A, GDR-M, GDR-T) placed in ESRS 2 itself, rather than repeated inside each topical standard. The XBRL taxonomy will need to be reworked to reflect this consolidation before it can be adopted. For a recap on the structure of ESRS 1 and ESRS 2, visit our companion article on the cross-cutting standards. For a recap on materiality, visit our article on double materiality.

Topical ESG Standards

= ESRS E1-E5 (Environment), ESRS S1-S4 (Social) and ESRS G1 (Governance)

The topical ESG standards present disclosures for companies to report on specific environmental (E1-E5), social (S1-S4) or governance (G1) topics. The topical standards partly reflect the Disclosure Requirements of ESRS 2 and partly cover Disclosure Requirements specific to a given environmental, social or governance matter.

For the ESRS XBRL taxonomy, the topical standards can be divided into:

1. ESRS 2-Related Disclosure Requirements

Linked to ESRS 2 IRO-1 (Impact, Risk and Opportunity), ESRS 2 SBM-3 (Strategy and Business Model) or ESRS 2 GOV (Governance). These can be thought of as extensions of ESRS 2 content that apply across topical standards. They are represented in this section of the XBRL taxonomy.

Exception: SBM-3 can optionally be disclosed in the reporting with the topical standards or with the ESRS 2 requirements.

2. Disclosure Requirements in topical standards

Linked to topical ESRS standards — Environment (E1-E5), Social (S1-S4) and Governance (G1). Disclosure Requirements within each topical standard are distinctly defined and labelled with numbers (e.g. DR E1-1). The associated information is digitised within each topical standard, reflecting disclosure requirements at a topical level.

Disclosure Requirements within each topical standard are distinctly defined and labeled with numbers (e.g., DR E1-1) in each corresponding ESRS. The associated information is digitized within each topical standard, reflecting disclosure requirements at a topical level.

EFRAG has released a Datapoint List in Excel format, which contains the complete list of all Disclosure Requirements and references on the basis of separable data points. This Datapoint List represents the basis for structuring the digital ESRS XBRL taxonomy and helps to get a first overview over the number and nature of data points that need to be reported.

For a recap on the (Draft) ESRS Data Points List published by EFRAG, visit our companion blog article: Decoding ESRS Data Points: A Practical Guide.

Understanding the Process: XBRL Tagging Explained

The ESRS XBRL Taxonomy comprises a set of XBRL elements (also called tags or "concepts"). Assigning these elements to reporting content is what's referred to as XBRL tagging. This is the process that — when the regime is operative — enables companies to identify, navigate and retrieve digital disclosures from the ESRS.

To read the "XBRL language" and open the XBRL taxonomy file provided by EFRAG, you need an XBRL software tool. software.xbrl.org lists certified tools that can process XBRL taxonomies. EFRAG also publishes a human-readable version of the XBRL Taxonomy in Excel for illustration purposes.

The XBRL taxonomy file shows folders ("roles" in XBRL language) that reflect the structure of the standards described above. Clicking on a single standard (for example ESRS E1-5) shows particular XBRL attributes — data types and dimensions related to that standard.

Data Types in the ESRS XBRL Taxonomy

The data types used in tagging sustainability statements cover quantitative formats (numerical disclosures) and qualitative formats (narrative or semi-narrative disclosures). The specific format of each data point is tagged accordingly when applying the taxonomy, as far as the company is able to automatically extract separable information.

Data types are:

- Numerical: quantitative data points, such as monetary amount, percentage or volume value.

- Semi-narrative: descriptive, comparable elements that can be associated with a specific category, such as a binary choice (boolean type: yes/no) or a dropdown value selection (enumeration type: item list).

- Narrative: text blocks providing qualitative information.

In the August 2024 draft, up to 70% of total ESRS data points were narrative disclosures. That figure is likely to drop in the revised standards: Directive (EU) 2026/470 mandates the Commission to prioritise quantitative over narrative datapoints, and the November 2025 EFRAG draft moves in that direction.

While numerical data points are highly comparable between companies, comparability decreases for narrative data points. Semi-narrative elements can be used to enrich otherwise unstructured narrative disclosures.

The amount of narrative disclosures underlines the nature of sustainability information, where, unlike financial statements, qualitative information in the form of narrative text does not simply complement monetary figures in the report. Instead, qualitative information is disclosed as a distinct element and has equal importance.

Dimensions in the ESRS XBRL Taxonomy

Dimensions in the ESRS XBRL Taxonomy

In addition to quantitative and qualitative elements, the draft taxonomy includes dimensions that allow disclosures to be broken down further.

There are two dimension types:

- Explicit dimensions — provided as a pre-defined list of elements (also called dimension members), such as country, gender, GHG type and so on.

- Typed dimensions — specific to certain entities and reported in their context, such as geographical areas, policies, targets and operating segments.

Example of the XBRL View (“Presentation Linkbase”)

The structured view of the ESRS XBRL elements inside the XBRL software tool is called the presentation linkbase. Each XBRL element has a unique ID in the system, is identifiable by its technical name and comes with a brief description of its labels. The elements are grouped according to the Disclosure Requirements and shown as a tree structure in the presentation linkbase view.

The linkbase clearly shows the relationships between the elements and their attributes. It shows the associated data types for each element and refers to the relevant places in the ESRS where the disclosure requirements are defined. Where applicable, links to other standards or EU legislation are shown too.

The image below illustrates the presentation linkbase for ESRS E1-5 (strongly simplified), with the quantitative and qualitative data points that would need to be reported for this standard.

Dimensions and other attributes that specify a certain standard will open up in an additional view when clicking on it.

Inline XBRL Tagging

A straightforward form of tagging is Inline XBRL (iXBRL). iXBRL offers a way to embed XBRL tags within HTML documents — combining the advantages of tagged data with a human-readable report format that can be viewed in a web browser.

iXBRL provides a verifiable way to convert narrative reports into facts in a generated XBRL document. iXBRL tagging is flexible and does not require disclosures to be presented in table structures.

As a result, iXBRL tagging enables the generation of sustainability reports that are both human-readable and machine-readable.

Note: EFRAG developed the ESRS Set 1 XBRL taxonomy labels in English only. Once tagging resumes, the European Commission will handle translation, adoption and publication in the Official Journal.

August 2024 Draft & Outlook to Resumption

EFRAG's changes since the first draft (historical context)

Following a round of feedback and Q&A, EFRAG revisited its 8 February 2024 draft and published a revised version on 30 August 2024. As described in the "ESRS Set 1 XBRL Taxonomy Explanatory Note and Basis for Conclusions," the changes included:

- Clarity of requirements: Added details specifying whether disclosures are mandatory ("shall"), voluntary ("may") or conditional (e.g. high climate-impact sectors).

- Calculation linkbases: Introduced for tables like ESRS 2 SBM-1 and E1-5 to ensure mathematical accuracy.

- Improved readability: Renamed boolean elements and clarified complex conditions using "and/or" formulations.

- Element splitting: Divided elements like "Name or ID" to enhance validation rules.

- Enhanced validation: Extended rules to cover phased-in provisions, optional tags and unit validations.

- Refined reporting scope: Added dimensions to distinguish facts such as targets, corrections, timelines and milestones.

- Centralised templates for targets: Consolidated non-adopted targets into central templates, similar to policies and actions.

- Sustainability topics categorised: Enumeration of all sustainability matters included in MDR tables.

- Expansion of G1 standards: Added MDR tags for policies, actions and targets under G1.

- Improved interoperability: Adjusted elements and dimensions to align with ISSB S1/S2 standards.

- Simplified text blocks: Removed overlapping narratives between ESRS 2 and topical standards.

- New dimensions: Reporting scope now reflects short-/medium-/long-term horizons and milestone-specific facts.

- Specific additions: Added elements for microplastics, target coverage and stakeholder involvement in target setting.

- Clarity on stakeholder involvement: New wording ensures stakeholders are involved for each material sustainability matter.

These changes informed the final draft submitted to the European Commission and ESMA in August 2024. The taxonomy now awaits ESEF amendment before it can be adopted as binding rules.

Path to Resumption

Mandatory tagging of sustainability reports is suspended until the ESEF Delegated Regulation (2019/815) is updated. The realistic sequence of events looks like this:

- Step 1: Commission adopts the revised ESRS delegated act (adopted 3 July 2026, based on the November 2025 EFRAG draft).

- Step 2: EFRAG reworks the XBRL taxonomy against the revised standards — in particular, the consolidated GDR-P/A/M/T structure in ESRS 2.

- Step 3: ESMA prepares draft Regulatory Technical Standards (RTS) for tagging.

- Step 4: Commission amends the ESEF Delegated Regulation (2019/815) to cover sustainability tagging.

- Step 5: Tagging obligation resumes. No firm date has been announced.

In the meantime, sustainability reports continue to be prepared in ESEF format but the sustainability portion is not subject to mark-up. Member States may also waive collective board responsibility for digital mark-up of sustainability information (amended Article 33(1)).

Related Draft Article 8 XBRL Taxonomy

EFRAG was also assigned to develop the Sustainability Reporting Digital Taxonomy for the Article 8 disclosure requirements under Delegated Regulation (EU) 2021/2178 (Article 8), which complements the EU Taxonomy Regulation. Information disclosed under Article 8 of Regulation (EU) 2020/852 will be included in the sustainability statement and tagged accordingly — once mandatory tagging resumes. Similar taxonomy features are employed in related taxonomies, such as the IFRS taxonomy, as disclosure standards and their digital models continue to evolve.

Get Ready for the Concept (Even While Tagging Is Suspended)

Even with mandatory tagging suspended, the data-structure logic of XBRL is still useful as a discipline. Separating each disclosure into a tag-able element supports clarity, auditability and a smooth transition once tagging resumes. ESG software like Sunhat can help by:

- Collecting the necessary qualitative and quantitative data for your disclosures in a structured way.

- Mapping data points to the relevant Disclosure Requirements (DRs) and Application Requirements (ARs) of the ESRS, so the structure is ready when tagging resumes.

- Keeping evidence and methodology alongside the data — the same structural discipline that XBRL tagging will eventually require.

With the right preparation, you can simplify the entire ESRS process, maintain compliance, and focus on presenting your sustainability story with confidence. Take a look at our ESRS module in a short demo: Book a demo

Stop scrambling. Start proving.

Your next customer questionnaire, assessment, or audit doesn't have to be a fire drill. Get the platform that keeps proof ready for every request.

Frequently Asked Questions

No. Directive (EU) 2026/470 (Omnibus I, in force 18 March 2026) amends CSRD Article 29d to suspend the mark-up obligation: "undertakings shall not be required to mark up their sustainability reporting" until the ESEF Delegated Regulation (2019/815) is updated to include sustainability tagging rules.

The ESRS XBRL Taxonomy, developed by EFRAG, is a digital model that allows companies to categorise sustainability data based on the ESRS in a structured, machine-readable format. Built on Extensible Markup Language (XML), it enables (when the regime is operative) companies reporting under the CSRD to tag and digitalise their sustainability disclosures.

The taxonomy is structured to mirror the ESRS framework: two cross-cutting standards (ESRS 1 and ESRS 2) and ten topical standards covering Environmental, Social and Governance (ESG) topics. It emphasises the interrelation between these standards so that all aspects of sustainability reporting are digitally accessible.

Two reasons. First, it's the EFRAG work that ESMA and the Commission will pick up once the ESEF rules are updated — it is in the queue, not in the bin. Second, the November 2025 EFRAG draft of ESRS 1 and ESRS 2 has changed the standards' architecture (notably the consolidation of MDR-P/A/M/T into GDR-P/A/M/T in ESRS 2), so the August 2024 taxonomy will need rework before any future adoption. Reading the existing draft remains useful for understanding the concept.

No firm date has been announced. The likely sequence is: Commission adopts revised ESRS delegated act (adopted 3 July 2026) → EFRAG reworks taxonomy against the revised standards → ESMA prepares RTS → Commission amends ESEF Delegated Regulation (2019/815) → tagging obligation resumes.

Yes. Omnibus I amends Article 33(1) of the Accounting Directive to allow Member States to waive the collective responsibility of administrative, management and supervisory bodies for the digital mark-up of sustainability information.

.avif)