Latest update on March 26, 2026

[cg_add-class=heading-style-h4]In a Nutshell

- Analyzing the materiality of a company forms the basis for understanding the impact of sustainability issues

- According to CSRD, companies must analyze double materiality: "Financial materiality" examines the risks and opportunities that affect the financial performance of the company, while "impact materiality" captures the impact on people and the environment

- Double materiality acts as a filter to exclude non-material topics, significantly reducing the reporting burden under the 2026 guidelines.

- This assessment is the mandatory starting point for CSRD reporting; it determines which ESRS standards you must disclose.

- Thresholds for materiality are determined by factors like scale, scope, and irremediability

Companies today are faced with a growing responsibility to act sustainably — transparent reporting, well-founded decisions and long-term strategies are essential for this. The first, fundamental step in preparing sustainability reporting in accordance with CSRD (Corporate Sustainability Reporting Directive) is to analyze the company's double materiality.

To support you on your company's double materiality assessment, the following guide delivers a compact overview of the key aspects relevant for your implementation in 2026.

What is the Concept of Materiality?

Materiality is the principle companies use to identify which sustainability topics are most important — or "material" — to prioritize in their business policies and reporting. A materiality analysis is a formal process of assessing a company’s activities to determine which specific information is essential for stakeholders to understand the company's performance.

According to EFRAG, materiality is assessed based on three core pillars:

- Significance of Information: How well the data depicts the actual environmental or social phenomenon.

- Stakeholder Expectations: The capacity of the information to meet the decision-making needs of both the company and its stakeholders.

- Public Interest: The general need for transparency regarding the company’s impact on society.

Understanding Double Materiality: The "Inside-Out" and "Outside-In" Perspectives

The CSRD requires a dual lens, often described as "double materiality." A topic is considered material if it meets the criteria from either the impact perspective, the financial perspective, or both.

- Impact Materiality (Inside-Out): This perspective captures how your company’s actions affect people and the planet. It includes actual or potential, positive or negative effects across your own operations and your entire upstream and downstream value chain.

- Example: For an airline, CO2 emissions are a material topic because their primary environmental impact is the greenhouse gases produced from flying.

- Financial Materiality (Outside-In): This lens focuses on how sustainability matters create financial risks or opportunities for your business. It includes factors that could influence your company’s future cash flows, financial position, or cost of capital over the short, medium, and long term.

- Example: For an big agriculture company, Climate change is a significant risk as natural disaster on the fields significantly impact the financial results.

Why 2026 Marks a Strategic Shift

Before the introduction of the European Sustainability Reporting Standards (ESRS), many organizations viewed sustainability through a single lens—either focusing on how environmental issues might affect their immediate profits or the Impact Materiality as part of other frameworks such as GRI. Under the 2026 guidelines, double materiality pushes reporting beyond a single sided disclosure into a comprehensive reflection of a company's interaction with the wider world.

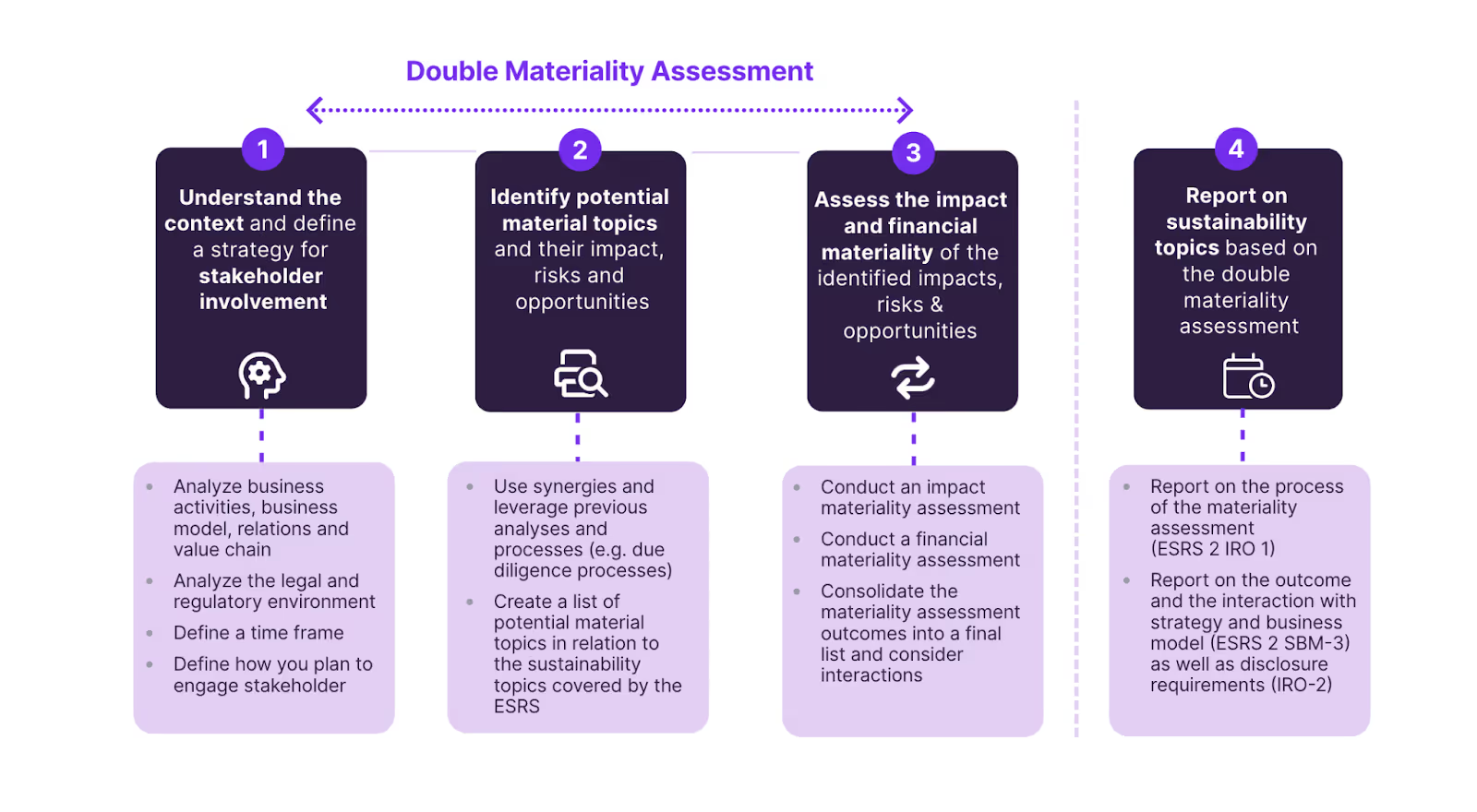

The Process: A 3-Step Implementation Framework

The double materiality assessment is a formal process designed to identify "material" ESG matters while excluding those that do not significantly impact your organization. According to EFRAG guidelines, this is not a "one-size-fits-all" exercise; it must be tailored to your specific business model, geographic locations, and value chain.

The Strategic Workflow

- Understand the Context: Map your company's activities, business relationships, and upstream/downstream value chain to set the scope for the assessment. Define a strategy for stakeholder involvement.

- Identify Potential Material Topics (IROs): Create a list of potential sustainability matters including topics, sub-topics, and sub-sub-topics and identify the related Impacts, Risks, and Opportunities (IROs).

- Assess Materiality and Set Thresholds: Apply objective criteria to your list. Evaluate Impact Materiality based on severity (scale, scope, and irremediability) and Financial Materiality based on the magnitude of financial effects and their likelihood of occurrence.

The 2026 Omnibus Perspective: ESRS E1 (Climate)

Under the latest guidelines, companies have more discretion to prioritize their reporting, but this increases the need for a robust audit trail. For example, if you deem ESRS E1 (Climate Change) non-material, you must provide a specific explanation of the criteria used to reach that conclusion.

Auditors and regulators (like BaFin) view Climate Change as "material by default" for the vast majority of sectors. A missing explanation or a generic "not applicable" statement is a high-risk trigger for non-compliance sanctions. Because of the heavy documentation requirement for a "non-material" conclusion, most companies find it more efficient and less legally risky to include ESRS E1 in their report.

Setting Thresholds & Assessing IROs

To determine which topics are included in your sustainability statement, you must apply objective thresholds to both your impact and financial perspectives. The goal is to consolidate these into one final list of material topics.

Actual negative impacts are evaluated based on their severity, which is determined by three mandatory factors: scale, scope, and irremediability. These impacts are typically categorized on a spectrum from low to high; any impact that exceeds your organization's defined materiality threshold is classified as a material topic that must be disclosed in your sustainability statement.

In practice, if any one of these three factors — scale, scope, or irremediability — is flagged as critical or significant, the impact is generally deemed severe and therefore material, regardless of the other two scores.

Once you have set your thresholds, you must apply them to the full scope of your business, which includes looking beyond your own direct operations.

The Value Chain: Extending Your Reporting Boundary

The CSRD requires companies to look beyond their own front door. A comprehensive materiality analysis must identify and assess Impacts, Risks, and Opportunities (IROs) across both your upstream (suppliers) and downstream (customers/end-of-life) value chain. Without this broader perspective, sustainability reports risk being incomplete, as many significant IROs occur beyond direct operations.

Mapping Your Involvement

When assessing the value chain, you must determine how your company is connected to a specific sustainability impact. Under the CSRD, your company’s involvement in sustainability impacts is categorized by its level of responsibility, which closely aligns with the GHG Protocol’s emission scopes. You are considered to be causing an impact when you are directly responsible for it, typically mapping to Scope 1 and 2 emissions; for instance, a factory burning natural gas for heat is directly causing those emissions. Contributing to an impact involves indirect influence through operational decisions or sourcing practices—such as purchasing palm oil that leads to systemic environmental issues—and can bridge Scopes 1, 2, or 3. Finally, you are linked to an impact simply through business relationships across your upstream or downstream value chain, which primarily aligns with Scope 3; a common example is a technology company being linked to the carbon footprint of third-party data centers it utilizes but does not control.

The Value Chain 3-Year Transitional Relief (2026 Update)

Collecting granular data from hundreds of global partners is arguably the most significant challenge of CSRD compliance. To address this, the 2026 Omnibus I Directive formalizes a three-year transitional relief period.

For your first three years of reporting, you may omit granular value chain data including Scope 3 emissions, if the information is not "readily available". During this time, you are required to describe your "reasonable efforts" to obtain the data and outline your action plan to improve data quality in the future. This period allows both reporting companies and their smaller suppliers the necessary time to build robust data-sharing infrastructure.

Alignment with Global Frameworks: The "Once-Only" Principle

To reduce the administrative burden on companies, the European Commission and EFRAG have prioritized interoperability with global standards like the Global Reporting Initiative (GRI) and the International Sustainability Standards Board (ISSB). In 2026, this is governed by the "Once-Only" principle, which aims to ensure that data collected for one regulatory requirement can be reused for others.

GRI vs. ESRS: Leveraging Your Foundation

While the ESRS is built on double materiality, the GRI framework traditionally focuses on Impact Materiality.

- Synergies: The definition of impact materiality in the ESRS is fully aligned with the GRI 3: Material Topics standard.

- The Transition: If your company already reports under GRI, you have a significant head start. To achieve CSRD compliance, you primarily need to integrate the Financial Materiality lens and ensure your disclosures meet the specific data point requirements of the ESRS.

ISSB (IFRS) vs. ESRS: Financial Alignment

For the financial perspective, EFRAG has worked closely with the ISSB to align the definition of financial materiality.

- Standard Sync: The assessment of financial materiality in ESRS 1 is designed to be consistent with IFRS S1.

- Focus: Both frameworks rely on "decision-usefulness" for investors, meaning a single assessment process can often support both IFRS and ESRS reporting.

Sustainability Due Diligence (CSDDD)

Your materiality assessment must also incorporate the outcomes of your sustainability due diligence processes, such as those required by the CSDDD or the German LkSG. Due diligence helps identify "hot spots" in your value chain, which serves as critical primary data for your impact materiality scoring.

Bridging the Gap: How Sunhat Facilitates Your Double Materiality Journey

The "Once-Only" principle is the key to managing the increasing data burden of the CSRD. By aligning your Double Materiality Assessment with global frameworks like GRI and ISSB, you ensure that every data point collected serves multiple reporting requirements, reducing redundancy and administrative costs

However, identifying your material impacts, risks, and opportunities is only half the battle. The true challenge lies in translating those results into an audit-ready sustainability statement without drowning in spreadsheets.

Your first steps for your Double Materiality Analysis should be:

- Identify the Gaps Between Your Current Sustainability Reporting & the CSRD Requirements

- Set Up a System for Data Collection Processes

- Start Early With Your CSRD Implementation Plan

Relying for this process on our in-house experts grants you full support with the latest regulations. Sunhat’s Collaborative Proof Platform facilitates this by automatically mapping your material IROs to the correct ESRS data points while building a traceable "Proof Library" that is audit-ready from day one. Don't let your materiality analysis become an annual burden. Transform it into a strategic capability that secures your legal compliance, market access and investor trust.

Start Your Materiality Analysis with Sunhat Today!

Stop scrambling. Start proving.

Your next customer questionnaire, assessment, or audit doesn't have to be a fire drill. Get the platform that keeps proof ready for every request.

Frequently Asked Questions

Double materiality is the concept where companies need to assess how their actions affect both people and the planet, as well as how sustainability issues can impact their financial situation. Essentially, double materiality is a way of determining important topics based on two facets: impact materiality and financial materiality.

A materiality assessment usually focuses on only one perspective, either financial materiality or impact materiality. Financial materiality focuses on issues that can impact a company’s financial performance (internal). Whereas, impact materiality focuses on how a company’s activities affect people and the environment (external). Double materiality assessment combines both perspectives by assessing the effects on your company’s financial performance and the company’s impact on the planet and people.

Yes, the Double Materiality Assessment (DMA) is the mandatory starting point for all companies reporting under the CSRD. It serves as the "filter" that determines which specific European Sustainability Reporting Standards (ESRS) are material to your business and must therefore be disclosed. If a company determines a topic is not material, they can omit those disclosures; however, for critical areas like Climate Change (ESRS E1), an explanation of why the topic was deemed non-material is legally required.

Sunhat’s Collaborative Proof Platform automates the most labor-intensive parts of the assessment by providing expert-led templates based on the latest ESRS and EFRAG data point lists. Instead of managing fragmented spreadsheets, teams can use Sunhat to dynamically scope their reporting—meaning once a topic is identified as material, the platform automatically activates the required Disclosure Requirements (DRs) and links them to the necessary evidence. This ensures a transparent, audit-ready trail that significantly reduces the manual effort required for compliance.

.avif)