Latest update on June 26, 2026

[cg_add-class=heading-style-h4]In a Nutshell

- The ESRS framework has two cross-cutting standards: General Requirements (ESRS 1) and General Disclosures (ESRS 2).

- ESRS 1 sets the concepts and principles — qualitative characteristics, double materiality, value chain, time horizons, and the phase-ins under ESRS 1 §125.

- ESRS 2 sets disclosures that apply across all sectors and feeds into every topical standard. In the November 2025 EFRAG draft, ESRS 2 introduces consolidated General Disclosure Requirements (GDR-P, GDR-A, GDR-M, GDR-T) that replace the per-topic MDR-P/A/M/T pattern.

- Find out more about the topical standards in our companion guides: ESRS E1-E5, ESRS S1-S4, ESRS G1.

The first set of ESRS were adopted on 31 July 2023 by Commission Delegated Regulation (EU) 2023/2772. Three years on, the legal anchor has shifted. Directive (EU) 2026/470 (Omnibus I, in force 18 March 2026) amends the CSRD and the Accounting Directive, and the Commission adopted the revised ESRS delegated act on 3 July 2026 (amending Delegated Regulation (EU) 2023/2772), based on the December 2025 EFRAG draft. It is now in the two-month European Parliament and Council scrutiny period; voluntary early application is permitted from FY 2026, with mandatory application from FY 2027.

This article walks through the two cross-cutting standards as they stand: ESRS 1 (General Requirements) and ESRS 2 (General Disclosures), reflecting the November 2025 EFRAG draft. We'll flag where the revised standards differ from the 2023 text.

ESRS 1: General Requirements

ESRS 1 outlines the general requirements for sustainability disclosure that apply to undertakings in CSRD scope. It does not stipulate specific disclosures — it sets the concepts, principles and architecture that every other ESRS plugs into.

In the November 2025 EFRAG draft, ESRS 1 has been shortened (around 32 pages, down from the 2023 version) and restructured. The key chapters cover:

- Categories of ESRS standards, reporting areas and drafting conventions.

- Qualitative characteristics of information.

- Double materiality analysis as the basis for sustainability disclosures — with the explicit materiality filter (§24) and top-down option (§27) added in the November 2025 draft.

- Due diligence procedure.

- Value chain information — including the new statutory value-chain cap and 3-year transition under amended Article 19a(3).

- Time horizons.

- Preparation and presentation of sustainability information.

- Structure of sustainability statements.

- Linkages with other parts of corporate reporting and connected information.

- Transitional provisions and phase-ins under §125.

Guiding principles for CSRD sustainability reporting

The objective of ESRS 1 is to set:

- the structure of ESRS

- the drafting conventions

- fundamental concepts

- the overall requirements for compiling and presenting sustainability information

in alignment with Directive 2013/34/EU as amended by Directive (EU) 2022/2464 (CSRD) and now further amended by Directive (EU) 2026/470 (Omnibus I).

ESRS 1 requires undertakings to disclose all material information about their sustainability-related impacts, risks and opportunities (IROs) in accordance with the ESRS standards. The November 2025 draft makes the materiality filter explicit:

Climate change is the one topic that carries heightened scrutiny. If an undertaking concludes that climate change (ESRS E1) is not material, the November 2025 EFRAG draft still requires a detailed explanation of how that conclusion was reached. In practical terms: "comply or explain" applies to E1 in a way it doesn't to other topical standards. The live blog's older claim that climate disclosures apply "regardless of materiality" oversimplifies what was always a comply-or-explain mechanism, and is now superseded by the explicit §24 filter.

The November 2025 draft also permits a top-down materiality approach (§27): undertakings can anchor materiality in their strategy and business model rather than starting from a bottom-up review of every IRO. AR 12 and AR 14 of the same chapter confirm qualitative analysis can be sufficient and that undertakings do not need to analyse every characteristic of severity or every time horizon.

Qualitative characteristics for information according to ESRS 1

When preparing the sustainability report in accordance with the CSRD, an undertaking must observe these quality characteristics:

Fundamental characteristics:

- Relevance: the information presented must influence the decisions of stakeholders.

- Faithful representation: information must reflect relevant facts accurately, completely and neutrally.

Enhancing characteristics:

- Comparability: information should be comparable across time periods and across other undertakings (especially in the same industry).

- Verifiability: independent, knowledgeable third parties could reach consensus — for example by disclosing inputs and calculation methods.

- Comprehensibility: any reasonable, knowledgeable stakeholder can readily understand the information.

Further detail in ESRS 1 Appendix B (preserved in the November 2025 draft).

Phase-ins under ESRS 1 §125

The November 2025 EFRAG draft replaces the previous 750-employee phase-in pattern with a new regime tied to Wave 1 reporters and the reporting period. Key reliefs:

- E4 (Biodiversity & ecosystems), S2 (Workers in the value chain), S3 (Affected communities), S4 (Consumers and end-users): may be omitted in full by Wave 1 reporters for financial years prior to FY 2027.

- E1-11 (Anticipated financial effects): phased to FY 2027 qualitative / FY 2030 quantitative.

- E2-5 substances of concern: quantitative disclosure phased to FY 2030.

- S1-6, S1-7 (non-EEA workers), S1-10..S1-14: phased to FY 2027.

These provisions exist because some data — especially value-chain worker data, biodiversity impact and community impact — is genuinely hard to measure in the current state of methodologies.

Stakeholder identification

ESRS 1 requires undertakings to identify two main stakeholder groups:

1) Affected stakeholders

Individuals or groups whose interests are or could be affected — positively or negatively — by the undertaking's activities and through its value chain. Under the new value-chain cap, small suppliers ("protected undertakings" with ≤1,000 employees) have a statutory right to decline information requests that exceed the VSME standard.

2) Users of sustainability reporting

Stakeholders with an interest in the undertaking, including:

- Primary users of general-purpose financial reporting: existing and potential investors, lenders and other creditors (asset managers, credit institutions, insurance companies).

- Other users, including business partners, trade unions and social partners, civil society organisations and non-governmental organisations.

Illustrative example: structure of an ESRS sustainability statement

ESRS 1 provides illustrative, non-binding examples of how an ESRS sustainability statement can be structured. The example below shows a company that has concluded — through its materiality assessment — that climate change, circular economy, own workforce, workers in the value chain, and consumers and end-users are material, while biodiversity and ecosystems, pollution, and affected communities are not material.

ESRS 2: General Disclosures

ESRS 2 sets the cross-cutting requirements for general disclosures that apply to every undertaking in CSRD scope — irrespective of sector — and feed into the topical standards. ESRS 2 is the centre of gravity for the framework: it carries the disclosure architecture that the topical standards (E1-E5, S1-S4, G1) plug into.

Two architectural changes matter post-Omnibus:

- Sector-specific ESRS empowerment (Article 29b(1), subparas 3-6 of the Accounting Directive) has been deleted by Omnibus I. There will be no mandatory sector-specific standards.

- In the November 2025 EFRAG draft, ESRS 2 introduces consolidated General Disclosure Requirements: GDR-P (policies), GDR-A (actions), GDR-M (metrics), GDR-T (targets). These replace the per-topic Minimum Disclosure Requirements (MDR-P/A/M/T) that the 2023 ESRS placed inside each topical standard.

The four reporting areas of ESRS 2

ESRS 2 organises disclosures into four reporting areas: Impact, Risk and Opportunity Management (IRO), Governance (GOV), Strategy (SBM), and Metrics and Targets (MT). The structure below reflects the November 2025 EFRAG draft. Per-topic MDR-* designations have been consolidated into the ESRS 2 GDR-* family.

1) Impact, risk and opportunity management (IRO)

The processes by which impacts, risks and opportunities are identified, assessed and managed through policies and actions.

Disclosure Requirements:

- IRO-1: Description of the processes to identify and assess material impacts, risks and opportunities.

- IRO-2: Disclosure requirements in ESRS covered by the undertaking's sustainability statement.

Cross-cutting General Disclosure Requirements (under ESRS 2 in the November 2025 draft):

- GDR-P: Policies adopted to manage material sustainability matters (formerly MDR-P, per topical standard).

- GDR-A: Actions and resources in relation to material sustainability matters (formerly MDR-A).

2) Governance (GOV)

The governance processes, controls and procedures used to monitor and manage impacts, risks and opportunities.

Disclosure Requirements:

- GOV-1: The role of the administrative, management and supervisory bodies.

- GOV-2: Information provided to and sustainability matters addressed by the administrative, management and supervisory bodies.

- GOV-3: Integration of sustainability-related performance in incentive schemes.

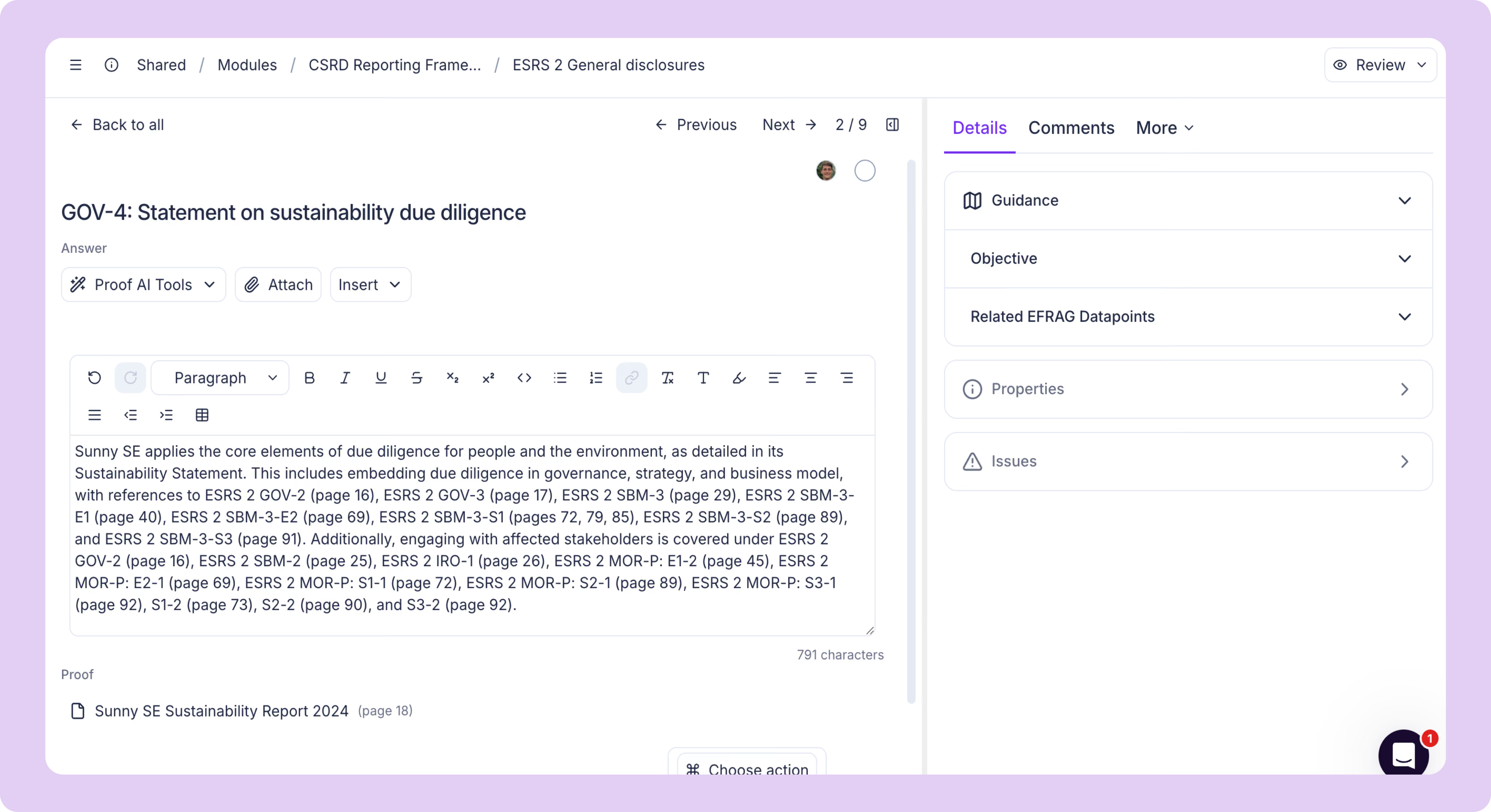

- GOV-4: Statement on due diligence.

- GOV-5: Risk management and internal controls over sustainability reporting.

3) Strategy (SBM)

How the business model and strategy interact with material impacts, risks and opportunities — and how the undertaking addresses them.

Disclosure Requirements:

- SBM-1: Strategy, business model and value chain.

- SBM-2: Interests and views of stakeholders.

- SBM-3: Material impacts, risks and opportunities and their interaction with strategy and business model(s).

4) Metrics and targets (MT)

How the undertaking measures its performance, including progress toward its goals and targets.

Cross-cutting General Disclosure Requirements (under ESRS 2 in the November 2025 draft):

- GDR-M: Metrics in relation to material sustainability matters (formerly MDR-M).

- GDR-T: Tracking effectiveness of policies and actions through targets (formerly MDR-T).

ESRS 2 is structured around a four-pillar system aligned with the climate-related disclosure framework formerly known as TCFD (Task Force on Climate-related Financial Disclosures) and now operationalised through IFRS S2 / ISSB (International Sustainability Standards Board). This alignment supports interoperability with global sustainability reporting standards — a direction the Commission must take account of, "to the greatest extent possible," when it revises the ESRS (recital 18(vi) of Directive (EU) 2026/470).

While ESRS 2 is mandatory for all undertakings in CSRD scope, the specific disclosure requirements that apply to each undertaking flow from its double materiality analysis, subject to the explicit materiality filter in ESRS 1 §24.

Learn more about the other ESRS

Read more in our companion blog posts:

Stop scrambling. Start proving.

Your next customer questionnaire, assessment, or audit doesn't have to be a fire drill. Get the platform that keeps proof ready for every request.

Frequently Asked Questions

The cross-cutting standards — ESRS 1 (General Requirements) and ESRS 2 (General Disclosures) — sit above the topical standards and give the overarching framework for CSRD reporting. ESRS 1 sets the concepts and principles (qualitative characteristics, double materiality, value chain, time horizons, phase-ins). ESRS 2 sets the disclosure requirements that apply to every undertaking, irrespective of sector, and feeds into the topical standards.

The original 2023 text is in Commission Delegated Regulation (EU) 2023/2772. The framework has since been amended by Directive (EU) 2026/470 (Omnibus I), published 26 February 2026 in OJ L. The Commission adopted the revised ESRS delegated act on 3 July 2026, based on EFRAG's December 2025 draft. Subject to Parliament/Council scrutiny, it applies from FY 2027 (voluntary early use from FY 2026).

Governance (GOV), Strategy (SBM), Impact, Risk and Opportunity Management (IRO), and Metrics and Targets (MT)

ESRS 1 sets overarching principles for ESRS reporting without specifying disclosure requirements. ESRS 2, mandatory for all undertakings in CSRD scope, outlines the disclosure requirements that apply universally to all sustainability matters — and feeds into every topical standard.

ESRS 1 is shorter (around 32 pages) and adds an explicit materiality filter in §24, a top-down materiality option in §27, and new phase-ins in §125 (E4 / S2 / S3 / S4 omissible by Wave 1 pre-FY 2027; E1-11, E2-5, several S1 DRs phased to FY 2027 or FY 2030). ESRS 2 consolidates the per-topic MDR-P/A/M/T into four cross-cutting General Disclosure Requirements (GDR-P, GDR-A, GDR-M, GDR-T). The four reporting areas (IRO, GOV, SBM, MT) are preserved.

In the 2023 ESRS, each topical standard carried its own Minimum Disclosure Requirements for policies (MDR-P), actions (MDR-A), metrics (MDR-M) and targets (MDR-T). The November 2025 EFRAG draft consolidates these into ESRS 2 as four General Disclosure Requirements (GDR-P, GDR-A, GDR-M, GDR-T). The result is one consolidated set that all topical standards refer back to, rather than repeated MDR-* sections inside each topic.

Heading

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

.avif)